ICANN survey shows that acceptance of domain name extension options is higher outside of the U.S. and Europe.

ICANN has released results of the first phase of a multi-year consumer study on the domain name landscape.

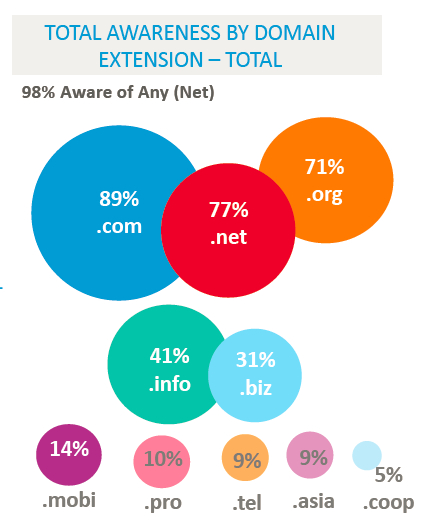

The survey of over 6,000 people who use the internet 5+ hours a week was conducted in February. Here are some of the notable findings around awareness and trust of top level domain names.

Awareness

Unsurprisingly, awareness in legacy domain names such as .com is much higher than new TLDs.

.Com dominated across all five regions — North America, South America, Europe, Africa and Asia. At least 88% of survey-takers were aware of .com. .Net and .org were also strong.

Other legacy TLDs, such as .info and .biz, had 18% to 50% awareness depending on the country. .Mobi, .Pro, .Tel, .Asia and .Coop had single digit awareness for the most part. (An outlier was .mobi in Africa, which has 40% awareness.)

When it comes to which legacy TLD someone would choose for setting up their own website in the next 6 months, .com also dominates.

Awareness of any of the new TLDs from a list of top sellers such as .email and .link was much lower. But here, an interesting trend emerges.

Only 29% of North Americans and 33% of Europeans were aware of any of the new TLDs they were shown. But 48% to 54% of people in South American, Africa and Asia were aware. This suggests those markets should be prime targets for new TLD registries.

The awareness and visitation stats on new TLDs get a little wonky, though. More people reported awareness of .email domain names than the other top domains. And of those that said they were aware of at least one new TLDs, 38% said they visited a .email website. This sounds odd, as .email isn’t really a site you’d think to visit as opposed to use in an email. It’s even more perplexing when people were asked which new TLDs they would consider to set up a website. .Email came in top at 50%, despite its specific nature.

ICANN also picked up on this anomaly. ICANN President of the Global Domains Division Akram Atallah noted:

The survey found that domains with an implied purpose and functional associations, such as .EMAIL, were most often recalled by Internet users. While some of the drivers may be linked to familiarity and general association versus awareness of the extension, we believe it’s a signal that people are receptive to the names.

I’d be very interested in free form response data about awareness of new top level domain names. For example, a question that asks people to list domain name extensions they’re familiar with, rather that showing an extension and asking if they are familiar.

Trust

People tend to trust things they’re familiar with, and domain names are no different. When shown individual legacy domain name extensions, they had an average “trustworthy” response of 90%. The number was even higher for targeted country code domain names at 94%.

When shown new TLDs, the numbers were much lower. The average trust in new extensions was 49%.

The survey only showed the top TLDs in terms of registrations as of the beginning of this year. There was quite a bit of difference in trust for each extensions.

.Email was the most trusted (non-geographic) new TLD at 63%. .XYZ and .guru had the least trust at 35% and 42% respectively. I find .email’s trust ratings interesting, as there are no restrictions on their registration.

You can view full results from the survey on ICANN’s website.

Here are some of the study conclusions (with my thoughts in parentheses) that support the Domain Name Industry.

– Trust in the Domain Name Industry is high: Low restriction and self policing may be made acceptable by the fact that the domain registration industry is seen to be at least as credible and trustworthy as other tech oriented businesses.

– The new TLDs that lead in awareness are those that appear to convey a purpose to the common user (i.e., semantic meaning)—the new TLDs carry a connotation of innovation.

– Only 88% of Internet Users, using Internet 5 or more hours per week, intend to visit a .com site in the next 6 months. (Really? 12% of relatively heavy Internet users won’t be visiting a .com site over the next six months?)

– Having a well-known extension is the most important factor in purchasing a domain name less than half the time (meaning people are open to new extensions). Price is an important factor. Short name availability is not much of a factor.

– Of those that used new extensions, 80% or more had Very/Somewhat Positive experience with new extensions.

– >80% favor light or no restrictions on purchasing domain names from new extensions.

– URL shorteners and QR codes are not showing widespread adoption, with Asia being a potential exception for QR codes.

– Consumers remember the actual web addresses for the sites they visit most often.

– Over 90% take charge of their own security by buying personal software or changing their Internet habits. <10% curtailed online purchases due to security concerns.

– Users would like to simplify the domain name registration process.

– A clear majority believe governments (police, consumer protection agencies, international agencies) are responsible for stopping abusive behavior.

Kurt Pritz

Domain Name Association

Kurt, good catch with only 88% of Internet Users visiting .com. Shows some sort of questioning or survey quality issue. I looked at the raw data and saw that the number also applies to the U.S. where 89% say they’ll visit a .com site.

In reviewing the actual questions Nielsen asked (on behalf of ICANN), one major problem emerges – or so it seems to me.

Asking people to write out a list of domain extensions they’re familiar with or have visited recently probably wasn’t feasible. For one thing, our recall of TLDs is incomplete. But the main reason that approach wouldn’t work is that important follow-on questions were tied to those initial lists. Most conclusions that can be drawn from those follow-on questions require uniformity.

But the problem I notice is that people are being prompted with these lists and will overestimate their own familiarity with TLDs simply because they’re staring at something that looks recognizable and plausible. Citing unexpectedly high numbers for .EMAIL, Nielsen itself admits “a pattern in this research that interpretability of the extension breeds a sense of familiarity”.

Nielsen ought to have added a certain number of bogus nonexistent domain extensions to their lists. That way, we’d have data concerning how frequently respondents unknowingly give false information after being asked leading questions. That baseline certainly isn’t zero. And it’s probably variable across countries and across possible domain extensions – meaning that, among TLDs that have never existed or haven’t launched yet, bogus recall rates will be higher for certain types than for others.

It would be good to know what percentage of people in various countries describe being familiar with .INTERNET and .AMAZON. How many of them have visited .PHONE and .USA websites in the past week? I’d like to know how likely they are to visit or register a .JESUS or .STOP or .AQUI or .MISR domain and compare their justifications with similar responses to real extensions.

Given such a baseline of spurious affirmative answers, we could properly interpret the remaining numbers in this study. Without it, we’re left guessing how much is real and how much is simply a reaction to the questionnaire.

@Joseph makes a good point “Nielsen ought to have added a certain number of bogus nonexistent domain extensions to their lists.”

Using such psychology as a “placebo” used in medical data, would have yielded a less biased result.

On non-US surveys, it’s clear to me that for ccTLDs that register on the 3rd level that respondents confused .com. with .com, assuming they are the same.

This is a great report because it’s incredibly early in the roll-out of new GTLD’s and 29% – 53% of respondents are familiar with them.

I think the “restrictions” on use question was inferred by respondents as “difficulty to use” which are barriers that will disappear over time as registrars make it easier to get and use names.

It’s nice to see .LINK gaining it’s rightful place at the top of the generic pile without Godaddy (marketing) support. Proof that you just can’t keep a viable name ending down. Consumers will get the products they want from the retailer that provides them.

I said from the beginning that .LINK will wind up as one of the top 3 or 4 largest name endings in the future. I feel even stronger about that after this report.

Long live .LINK

Frank, I don’t believe that’s correct – to say that 29-53% of people are familiar with the nTLDs. I have yet to meet a single person outside the domain industry who is genuinely familiar with them; and I personally still am not, since I regularly find myself looking up keywords in my database just to verify whether or not they’re actually being offered as new TLDs. Memory plays tricks.

Familiarity is a greater claim than awareness. And even awareness is far below 29-53%. The average awareness reported by this study is 1-18%.

You can verify that by looking at the first page of their “Summary of High Level Metrics”, which is entitled “Average Awareness and Visitation”. Here is a copy-and-paste version:

LEGACY TLDS TOTAL

AVERAGE AWARENESS (%)

.com, .net, .org

79% (74%-89% across regions)

.info, .biz

36% (31%-45% across regions)

.mobi, .pro, .tel, .asia, .coop

9% (5%-12% across regions)

Geographically Targeted TLDs (based on only those shown in that region)

86% (52%-95% across country)

versus

NEW TLDS TOTAL

AVERAGE AWARENESS (%)

Generic Extensions

14% (8%-17% across regions)

Geographically Targeted TLDs

7% (1%-18% across country)

Just to clear up the ambiguity, those 29-53% figures come from a section in the report entitled “Awareness of New TLDs” (about 31 pages in).

Take North America as an example. Here respondents said they were aware of nTLDs as follows:

2% .XYZ

3% .PHOTOGRAPHY

5% .CLUB

6% .GURU

7% .REALTOR

14% .LINK

16% .EMAIL

The 29% percentage means 71% of respondents were unaware of all of those nTLDs, whereas 29% were aware of at least 1 out of the bunch. Being aware of just 1 out of that set and unaware of the rest doesn’t constitute familiarity nTLDs.

In other words, people were shown a list of nTLDs and were unaware of the majority of them, but 29% circled at least 1.

That percentage was 33% for Europe, 48% for Africa, 53% for Asia, and 54% for South America. But, again, that’s minimal awareness – i.e. any single nTLD circled out of a big list of nTLDs. Awareness of individual nTLDs was much lower.

For instance, .XYZ peaked at 7% in Asia but was 2% in Europe and North America. .LINK ranged from 13% in Europe to 37% in South America. It was 28% in Asia. The global average seems to be 24% .LINK versus 5% .XYZ.

And that’s significant. .XYZ is touted as the most registered nTLD, with several times the volume of .LINK; yet awareness of that suffix lags behind .LINK by a factor of 4 in Asia and a factor of 7 in every other continent.

Mysterious, no?

So Joseph.. Familiarity and awareness are obtuse metrics which mean different things to different people. I started out in my post high-school days as a market research poll conductor and I know a little about these types of surveys and the pattern of confusion which can sometimes result. In short “nobody knows nothin” but you can learn a lot by divining patterns from the tea-leaves.

In these early days of the GTLD program, as a registry operator, I’d be pleased with 1-2% of either (familiarity or awareness). I’m giddy with 29-53% of either. In hindsight I shouldn’t be surprised that internet power-users are familiar or aware, as it relates to new gtld’s because web-wide (at registrars, and in the press) the marketing for new name endings has been thick and wide. Hardly a day goes by in the main-stream press without a story about .SUCKS .CARS .other stuff.

Registration is entirely another matter and can be inflated by single registrants of premium names, registry reservations or methodical “placement” of names in existing registrar accounts. My dear colleagues at .xyz have taken other registry operators to college and done an unquestionably masterful job placing registrations with people and building a lasting meme in the hearts and minds of consumers with their new .xyz name ending (and others).

Marketing, while excellent (in the case of .club or .xyz) doesn’t negate human behaviour, which is a much more difficult ship to turn. Anything can be marketed, at some cost, but it’s much more difficult to sway what people believe and feel in their soul. This is the moment where human behaviour, art and science behind naming intersect – and, i suppose, the point of this poll. Nielsen, polled more than 6000 people worldwide, and this is what they “believe”.

Doubt it at you peril. The cream rises and the cream of the future will be .LINK, and .SHOP and .WEB when they finally launch and join .LINK at the TOp of the new generic pile. Other strings will have to pay more for their place n the top-ten, if they get there at all.

Naming is exactly the same as it ever was in the .COM world. The cream rises in old and new names.

.link, it says #1 country is where you live Cayman Islands. Top of generic pile? C’mon

https://namestat.org/link

@Frank,

As far as .LINK goes, it probably will rise to the top compared to many other generic nTLDs. That has been my own publicly expressed opinion for more than a year, in spite of my having registered only 1 .LINK domain out of the 1000-2000+ nTLD domains I’ve experimented with.

And the poll seems to bear that out to some degree. .LINK follows .EMAIL as the new TLD respondents said they were most aware of.

Methodologically, the Nielsen survey has some fundamental problems and limitations. For the reasons I outlined above, people should be expected to give spurious affirmative answers when prompted with familiar-looking extensions (real or imaginary). So awareness will be overestimated, and the overestimates will be greater for some TLDs than for others.

.EMAIL and .LINK are likely to experience the greatest distortion in self-reported consumer awareness because they’re common internet-related terms and look like plausible suffixes for domains. Yet even if the awareness figures for those TLDs are exaggerated, they would be exaggerated by actual consumers. And that’s very meaningful. It means that consumers perceive these TLDs as somehow more relevant, appropriate, or plausible.

If I were you, Frank, the figure I would concentrate on isn’t the 29-53% awareness of SOME nTLD. Rather, it’s the huge lead in awareness .LINK experiences over other nTLDs. At 14% awareness in North America, that’s more than double .GURU (which had the advantage of being first out of the gate), nearly 5 times .CLUB (which has had the best marketing), nearly 5 times .PHOTOGRAPHY (which has seen a surprising amount of adoption among photographers), and 7 times .XYZ (which manipulated the system to gain the most registrations). Those are numbers in this independent survey that you could actually leverage more to your advantage than the 29-53% figure (which looks much less impressive under scrutiny and which masks the lead enjoyed by .LINK).

I’d still say the 3 big ones are com, net, and org. Not to mention, there is still plenty of names to be had with these extensions. For instance, urhot.net is on Flippa at $1 right now with no reserve. https://flippa.com/4506501-great-domain-name-with-huge-potential-spin-it-however-you-like-top-keywords

I’m sure people *think* they’re familiar with .email domains because they’re confusing the domain and web address with email and email addresses. I.e., people are stupid and are going to assume they’ve “visited” a .email website simply because they’ve visited an email website and/or use email.