ICM acquisition and focus on renewal revenue help improve the picture at MMX.

There are a couple of warning signs that a top level domain name company is on shaky ground. One is if it’s dependent on one-time premium sales. The other is if it’s dependent on China for most of its revenue or growth.

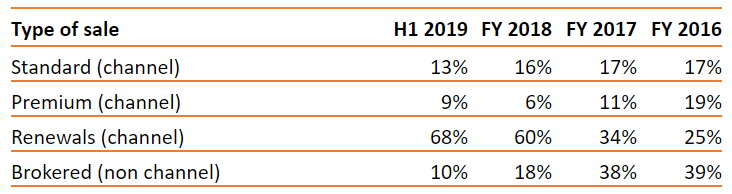

Both of these applied to MMX (Minds + Machines) (London AIM: MMX) in the past. So two charts in the company’s earnings release yesterday for H1 2019 are important.

The first shows that reliance on one-off premium sales has decreased:

During this time, revenue (not including one-time gains) has been fairly steady, so this is a real improvement. It’s not that everything has gone down with some taking more of a hit than others.

Sure, a big driver of this change was the acquisition of ICM Registry including .xxx. It wouldn’t have happened this quickly with the existing TLD portfolio. Nonetheless, this paints a picture of company that now has healthier revenue. No hamster-wheel games of selling enough premiums to hit numbers.

MMX CEO Toby Hall has long preached the importance of covering operating costs with renewal revenue. The company’s goal is for renewal revenue to surpass OPEX, Cost of Sales and Partner Payments within the next 12 months.

As for China:

This chart shows the first half of each year and it could be a bit misleading. Last year China accounted for 29% of revenue, so Chinese revenue was front-loaded that year. But in 2017, China accounted for more than half of the company’s revenue. So any way you slice it, it is relying less on China.

The company has healthier revenue. Now it needs to find a way to grow faster.

Leave a Comment